Join our community of entrepreneurs and receive exclusive content!

The Illusion of Precision in Business Valuation

Valuation is often presented as a number. In practice, it’s a system of assumptions, sensitivities, and trade-offs. This piece explores how small changes in assumptions reshape outcomes and why understanding the drivers matters more than the number itself.

THINKING & INSIGHT

Juan Diego Londoño

4/20/20264 min read

What’s more dangerous than a bad valuation?

A precise one.

A model that returns a value of $10,482,317 feels authoritative. Clean. Defensible. Final.

But change one assumption, just one, and the number moves. Sometimes materially. Sometimes more than we’d expect.

Here's the uncomfortable truth: that number is, in large part, a construction. And the precision that makes it feel authoritative is often the very thing that makes it dangerous.

Precision creates comfort. And in valuation, comfort is often mistaken for truth.

Discounted cash flow models, comparable company analysis, transaction multiples; these are legitimate, rigorous tools. They are necessary. They give structure to ambiguity. They force us to articulate assumptions: growth, margins, reinvestment, discount rates.

But here’s the issue: these tools produce outputs that look exact, even when the inputs are anything but.

A terminal growth rate moves from 3.0% to 3.5%.

The discount rate shifts 100 basis points.

Margins normalize slightly higher or slightly lower.

Individually, these seem like minor adjustments. Collectively, they reshape the valuation.

And yet, the output is presented as a single number.

Clean. Polished. Convincing.

The client sees a conclusion, while the analyst is navigating a distribution.

That gap is where risk lives.

How precision turns into misinterpretation

A clean number carries implicit authority. Clients read a valuation report and process the figure the way they process a price tag: as a fact. The analytical apparatus behind it (i.e., the sensitivity tables, the scenario overlays, the footnoted assumptions) gets skimmed, rather than read and integrated. What sticks is the headline.

This dynamic creates two structural risks that rarely get named directly.

Risk 1: The analyst underestimates uncertainty

Even technically sound models carry hidden fragility.

A 1% shift in the discount rate can move a valuation by 20–30%.

A change in the terminal growth assumption (one number, usually embedded quietly) can swing the result by a similar magnitude.

These are not edge cases. These are the levers that drive the output.

When analysts present a point estimate without adequate sensitivity framing, they are, intentionally or not, compressing uncertainty into a signal that appears more stable than it really is.

Risk 2: The client interprets the output as truth

Buyers use valuations to justify acquisitions.

Founders use them to anchor fundraising conversations.

Boards use them to approve decisions.

In each case, the number becomes a reference point, and reference points are extraordinarily hard to dislodge once set.

A client who receives a valuation of $12.4M does not naturally think:

"This estimate could reasonably range between $9M and $16M, depending on which scenario materializes."

They think:

"We are worth $12.4M."

The decimal reinforces the conviction.

This is not a failure of intelligence. It is a failure of how the analysis is structured and communicated.

THE DCF SENSITIVITY PROBLEM

Consider a standard DCF for a mid-sized private company:

Revenue growth: 6% vs. 8% over the next five years

FCFF/Revenue: 18% vs. 20%

Discount rate: 11% vs. 12%

Terminal growth rate: 2.5% vs. 3.0%

None of these ranges are extreme. They are all defensible.

But run the model across these combinations, and you don’t get a tighter answer. You get dispersion. A wide one.

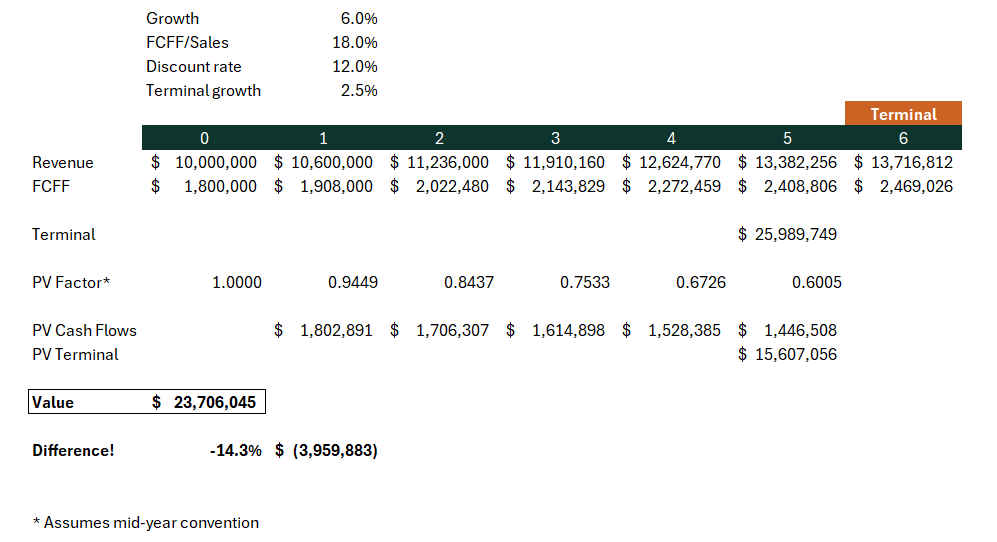

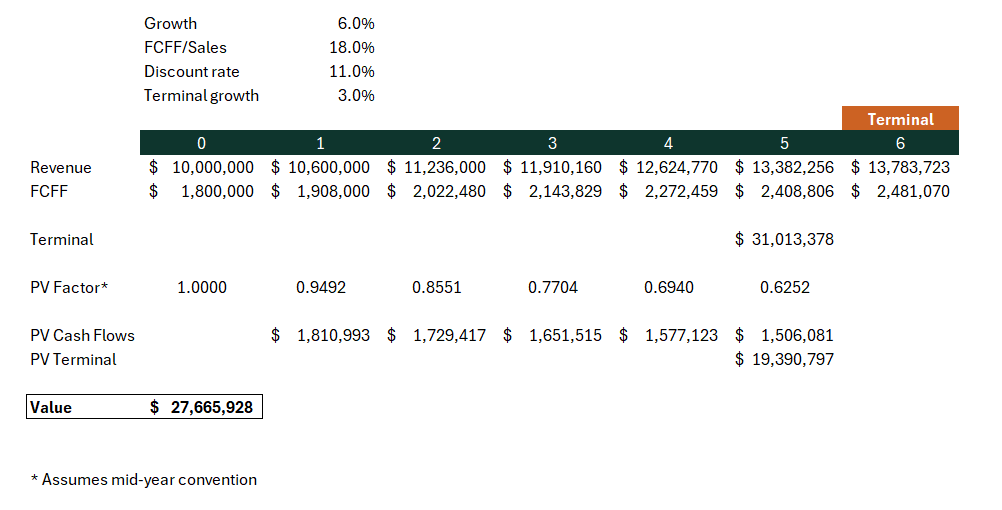

Now, take a base case:

6% revenue CAGR on a $10M base

WACC of 11%

Terminal growth of 3%

Output: $27.67M

The appearance of precision is not the same as accuracy. In valuation, confusing the two is not a minor error. It shapes decisions worth millions.

Now, adjust two inputs within reasonable estimation error:

WACC → 12%

Terminal growth → 2.5%

New output: $23.71M

That is a 15% reduction, or to avoid relativity bias: almost $4M left on the table!

The real takeaway

A good valuation doesn’t aim to be precise. It aims to be transparent.

Transparent about assumptions.

Transparent about ranges.

Transparent about what matters (and what doesn’t).

Valuation is not about being right in a static sense. It’s about mapping the terrain.

Where are the cliffs?

Where is the margin of safety?

What needs to go right for this to hold?

That’s the real output.

Next time you see a valuation, ask one question:

What had to be assumed for this number to exist?

The analyst's real deliverable is a framework for making sense of the range of plausible futures, so the decision-maker can act with clarity.

Same company. Same underlying business. Different points on an assumption curve.

The issue is not which assumption is correct. The issue is that presenting only the first number, without showing the distribution of plausible outcomes, is analytically incomplete.

It answers the wrong question.

From analysis to narrative

Now layer in real-world frictions:

Limited visibility on forward demand

Customer concentration risk

Execution risk in scaling operations

Marketability discounts for private ownership

The model becomes less of a calculator and more of a lens.

Yet in practice, what often gets delivered is a point estimate (sometimes with two decimal places) as if uncertainty had been resolved rather than framed.

This is where valuation quietly shifts from analysis to storytelling.

And the narrative tends to stick longer than the assumptions behind it.

The narrative that sticks

In M&A processes, buyers and sellers routinely enter negotiations anchored on valuation figures that were generated under specific (often optimistic) assumptions. When those assumptions do not materialize post-close, the purchase price still reflects them.

The number outlasted the logic behind it.

This is not hypothetical. It is a recurring pattern:

Synergies not properly stress-tested

Growth projections treated as base cases

Valuation ranges collapsed into a single negotiating anchor

And once the anchor is set, the discussion rarely returns to first principles

What appraisers are really delivering

There is a version of this work that prioritizes the comfort of the client: give them a number, give them confidence, move on.

And there is another version that prioritizes their decision-making: give them a range, show them the levers, make them understand what they're actually betting on.

I’ve come to see valuation less as an answer and more as a system.

A system that organizes uncertainty, tests sensitivity, and translates assumptions into implications.

When we reduce that system to a single number, we lose most of its value.

Worse, we create a false sense of certainty for the client… and sometimes for ourselves.

Uncertainty is not the problem. Hidden uncertainty is, so a good valuation does not aim to eliminate uncertainty but to map it.

Contact

contact@emporioadvisory.com

(+57) 310 530 0586

Social Media

Join our community of entrepreneurs and receive exclusive content

© 2026 Emporio Advisory. All rights reserved.