Join our community of entrepreneurs and receive exclusive content!

What Current Market Conditions Mean for Small and Mid-Sized Businesses

Inflation, interest rates, consumer behavior, and geopolitical uncertainty affect businesses through specific operational channels. This article explores how macroeconomic forces filter into pricing, working capital, margins, and growth decisions, helping business owners translate economic headlines into practical actions.

CONTEXTMARKETS

Juan Diego Londoño

6/21/20267 min read

Translation success: understanding where pricing power actually existed.

Translation failure: assuming cheap debt would remain cheap.

If your business model depends heavily on tomorrow, good news! Today just got harder.

Translation success: recognizing that valuation frameworks had changed before investors told them.

Inflationary pressures. Rate hikes. Tight labor markets. Geopolitical uncertainty.

Turn on any financial news channel, literally any, and you will hear the same narrative. Apocalyptical headlines in plain language for a mass audience, but abstract narratives and a shameful lack of depth.

What exactly does it mean for a business when “the market tightens”?

We are all in the same ocean, and the conditions that are leading a leveraged competitor to bankruptcy are the same ones building up strategic advantages for others. Although the economy does not give us a crystal ball, it gives us the tools to translate blurred signals and shallow headlines into decision rules for survival or conquest.

Stop asking if macro conditions affect your business (which is otherwise a very deep question in academic circles), and start asking yourself:

“Do I understand the specific channels through which rates, inflation, and instability land on my P&L, my cash conversion cycle, and my customers' wallets?”

One headline. Many narratives?

There is a persistent gap between how macro conditions are discussed in financial media and how they actually affect operators running a company with 20, 80, or 350 employees.

Economic commentary tends to live at 30,000 feet: GDP growth, central bank forward guidance, yield curve inversions… Useful signals, certainly, but they arrive pre-digested and abstracted, or in the best of the cases, contextualized in an environment that is not yours.

What most operators are missing is the translation layer: the mechanism that connects the Fed funds rate to their cost of receivables financing, or that links consumer credit tightening to an uptick in payment deferrals from their own clients.

In the middle of the disconnection, most small and mid-sized operators make one of two mistakes. Either they ignore macro entirely (“we just focus on what we can control”) or they panic reactively (“the news says recession, so we freeze spending”).

Both are costly.

The first mistake leaves you exposed. The second leaves you paralyzed.

I am not sure if “the right” narrative exists, but if it does, it must sit in between: extract structural signals from the noise, then translate those signals into specific and proportionate actions.

The current landscape. Crisis or opportunity?

Right now, three macro forces have caught my attention. They are far from new, atypical, or exceptional; however, their combined effect on working capital, pricing power, and business sustainability deserves some attention. Together, they configure an inflection point that many businesses have not yet priced into their operational assumptions.

Force 1. Energy & Geopolitical Pressures Driving Inflation

Rising oil and fuel costs linked to instability in the Middle East are creating a familiar problem: supply-side inflation.

Energy remains one of the economy's foundational inputs. When transportation, fuel, electricity, and logistics costs rise, the effects disseminate through supply chains very quickly.

For operators, it does not show up as a single dramatic shock.

Instead, it arrives through dozens of small adjustments:

Higher freight and shipping expenses.

Increased packaging and raw material costs.

More expensive agricultural inputs and fertilizer.

Supplier price revisions with shorter notice periods.

Greater volatility in procurement budgets.

Some inputs reprice immediately while customer contracts, pricing agreements, or competitive dynamics delay the ability to pass those increases forward. The result is margin compression: expenses adjust faster than revenues.

Businesses with weak pricing power feel this first.

Businesses with concentrated suppliers feel it next.

Everyone else eventually notices through working capital pressure and planning uncertainty.

There is also a second-order effect that receives less attention. Higher energy costs function like an indirect tax on consumers. More money spent on transportation, utilities, and essentials leaves less room for discretionary purchases. Even companies far removed from commodity markets can experience weaker demand as customers re-prioritize spending.

Suggested Action: Identify your three largest cost categories and determine which are directly or indirectly exposed to energy prices. Then model the impact of a 5%, 10%, and 15% increase in those inputs. If you cannot quantify the effect, you cannot manage it.

Force 2. The price of time has increased

When rates rise or remain elevated for a long time, the implicit “discount rate” applied to every business decision goes up.

Future cash flows are worth less.

Delayed profitability is penalized.

Working capital inefficiencies become visible.

What used to be sold as a “growth story” five years ago becomes a “timing problem” nowadays.

Final one: the growing startup seeking capital. Right after the pandemic, in the cheap-money era, growth solved everything (remember the rebound effect we observed in the economy after the lockdowns).

A few years later when the capital became scarce (signal), investor were hesitant to buy the growth story and started to ask about burn, payback periods, and unit economics.

The underlying business barely changed: customer acquisition remained healthy, retention was strong, and revenue continued to grow, but the market was not willing to pay the same price for that narrative. Investors stopped asking, "How fast can this grow?" and started asking, "How efficiently can it grow?"

The same solid subscription-based model, but now judged with a different lens. In this case, the market did not change the fundamentals, but changed the questions.

Another case: a small coffee roaster with three retail locations.

They saw inflation in green coffee beans and dairy (the signal).

Their first instinct was to raise prices across the board (the reactive panic).

We ran the elasticity analysis (the translation layer).

Turns out, their espresso drinks were inelastic (regulars would pay), but their bagged coffee sold to grocery stores was highly elastic (retailers would switch to cheaper brands). So they raised café prices 8% and kept wholesale prices flat. Total gross margin improved 4 points. No lost wholesale accounts. That is granular translation, and in this case, it led to a favorable outcome despite the harsh economic environment.

Rates may ease eventually, they always do, but the era of free money is structurally over. For SMEs, this means debt service becomes a sizable cost again. Lines of credit, revolving facilities, equipment financing, all of it is more expensive than it was three or five years ago. A business that grew using leverage without stress-testing its interest coverage is now finding that the margin for error is much thinner.

Suggested action: Model your interest coverage ratio at current rates plus 200 bps. If it stays well above your bank’s threshold, fine. If it drops below, take a closer look. Do not wait.

Force 3. Diverging Consumer Spending Patterns

Contrary to the dramatic narrative in media and popular culture, most markets are not uniformly shrinking. Actually, markets are fragmenting:

Consumers and clients are becoming more selective.

Budgets are tighter, but the underlying needs are still there.

Spending shifts toward perceived value and away from optionality.

A fragmented market creates a dangerous illusion: Revenue may hold at nominal value, but quality deteriorates (lower margins, harder sales cycles, higher acquisition costs).

Consumer and business spending has not collapsed because of the higher rates (or at least not evenly across income segments), but buyers are facing real trade-offs.

In B2B, for example, this shows up as longer sales cycles, more negotiation on terms, and higher churn risk in subscription or retainer-based models. The businesses feeling this most acutely are those whose value proposition was never sharply defined: those that competed on price during the expansion, rather than on genuine differentiation.

Customer price sensitivity has bifurcated. Lower-income segments are trading down. Upper-income segments are still spending, but they expect real value for their money.

Suggested Action: Audit your product mix. Which items have elastic demand? Those need cost discipline or value-add. Which are inelastic? Those can sustain selective price increases. Do not apply a blanket pricing strategy.

The translation layer in practice

There are several cases in which the observance or inobservance of the translation principles hereby exposed, led to favorable and disastrous outcomes, respectively. I have collected a few relevant ones:

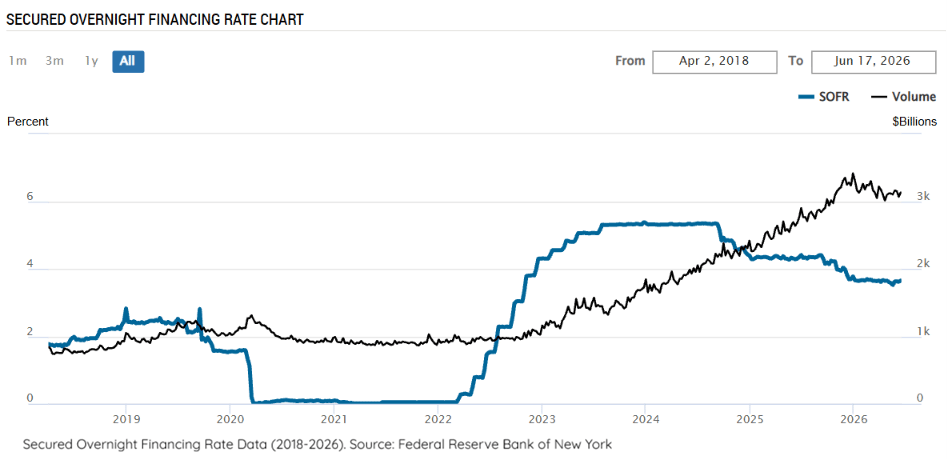

We were working with a distribution company in Alabama, USD 12 million in revenue. They had a floating-rate line of credit at SOFR + 3%. When rates were 0.8%, they paid 3.8%. No problem. When rates hit 5.3%, their effective rate jumped to 8.3%. Interest expense doubled. Their EBITDA coverage ratio dropped below the bank’s covenant limit (1.5x). The increase in rates did not happen overnight (despite what the acronym might suggest), it started compounding quietly, then exponentially, and finally the problem was unavoidable. Management continued ignoring the signals thinking the higher interest expense was a temporary inconvenience rather than a structural change, until it became too late. By the time the covenant breach occurred, the bank had already become the primary decision-maker.

A closer look into the transmission mechanism

In my work with business operators, the most common mistake I see is treating the current economic environment as something temporary: a cycle to be waited out rather than a regime to be adapted to.

The line of thinking is: if we hold on, conditions will normalize, and our cost of capital, our customers' purchasing behavior, and our competitive landscape will return to something familiar.

I think many operators misread the economic environment because they look for dramatic breaks instead of gradual and compounding shifts. Markets rarely announce regime changes as dramatic headlines in the news. Changes in economic conditions "filter" into business operations, often with subtle discretion, until the new regime is set up.

A slightly longer sales cycle here.

A slightly lower margin there.

A slightly more expensive line of credit.

Individually, each "slight" change is manageable (or at least visible), but together, they reshape the economics of your business (and that configuration is often invisible... until it is not).

The macro environment may not change the fundamentals of a good business. But it does change the score, and sometimes the whole scoring system.

Operators who understand the specific channels through which the economy filters into their business model are not just better at managing risk. They make better decisions on pricing, capital allocation, and growth timing.

That is financial analysis applied where it actually matters: inside the business.

The bottom line

Macro conditions are like the weather. You cannot change them or know them beforehand, but you can decide whether to go out in a storm without a coat.

Current market conditions, as described in this article, are not inherently good or bad. They are just different. The winners will not be the ones who predicted the future. They will be the ones who built a decision framework that works across a range of futures.

Do you have a routine process for taking a rate move or an inflation report and converting it into a change in your inventory policy, your collection terms, or your hiring plan?

Most do not. They read the news, feel anxious, and do nothing. Or they overreact and cut something that should have been protected.

If you had to stress-test your business under these conditions today:

Where does cash get trapped?

Where are margins quietly leaking?

What assumptions only worked in a cheaper-money environment?

Which decisions are we making today based on conditions that no longer exist?

Start there and tell me where you land.

Contact

contact@emporioadvisory.com

(+57) 310 530 0586

Social Media

Join our community of entrepreneurs and receive exclusive content

© 2026 Emporio Advisory. All rights reserved.